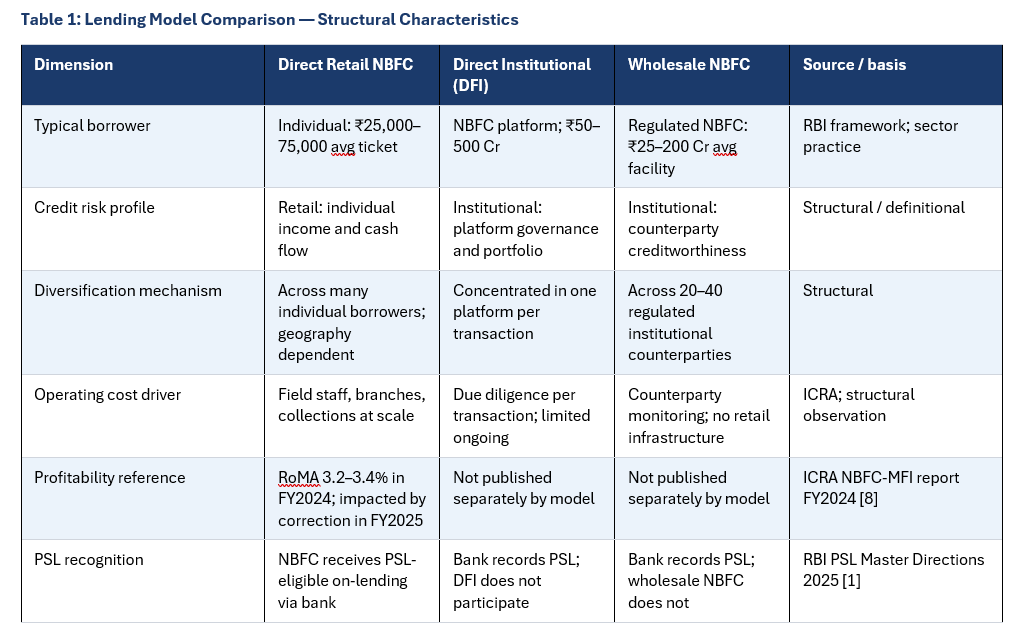

This is not a criticism of retail lending. It is an observation about its structural characteristics. An NBFC-MFI that has built a portfolio of ₹500 crore serving 200,000 borrowers across fifty branches has achieved something genuinely difficult. The field staff, the borrower relationships, the community knowledge, the collection discipline – none of that is easily replicated. But doubling that portfolio to ₹1,000 crore requires a near-proportional expansion in field staff, branch infrastructure and monitoring capacity. Some operating leverage emerges in mature geographies where branch density is already high, but new-geography expansion resets the cost base. The structural relationship between portfolio growth and headcount growth remains tighter in retail lending than in institutional lending models.

The wholesale lending model faces a different scaling equation. Its counterparties are not individual borrowers. They are regulated NBFCs, each with their own management teams, governance structures, audited financials and regulatory compliance obligations. Doubling the wholesale portfolio from ₹500 crore to ₹1,000 crore might involve adding five or six institutional relationships rather than 200,000 new borrowers. The analytical work of underwriting those relationships is intensive, but it does not scale linearly with portfolio size in the way that retail origination and field monitoring does.

This difference in scaling characteristics is the central argument of this paper. It does not mean wholesale lending is easier, or that it requires less analytical skill. It means that the relationship between portfolio growth and operational cost growth is structurally different, and that difference has consequences for how much capital the wholesale model can efficiently absorb and how it behaves under different market conditions.

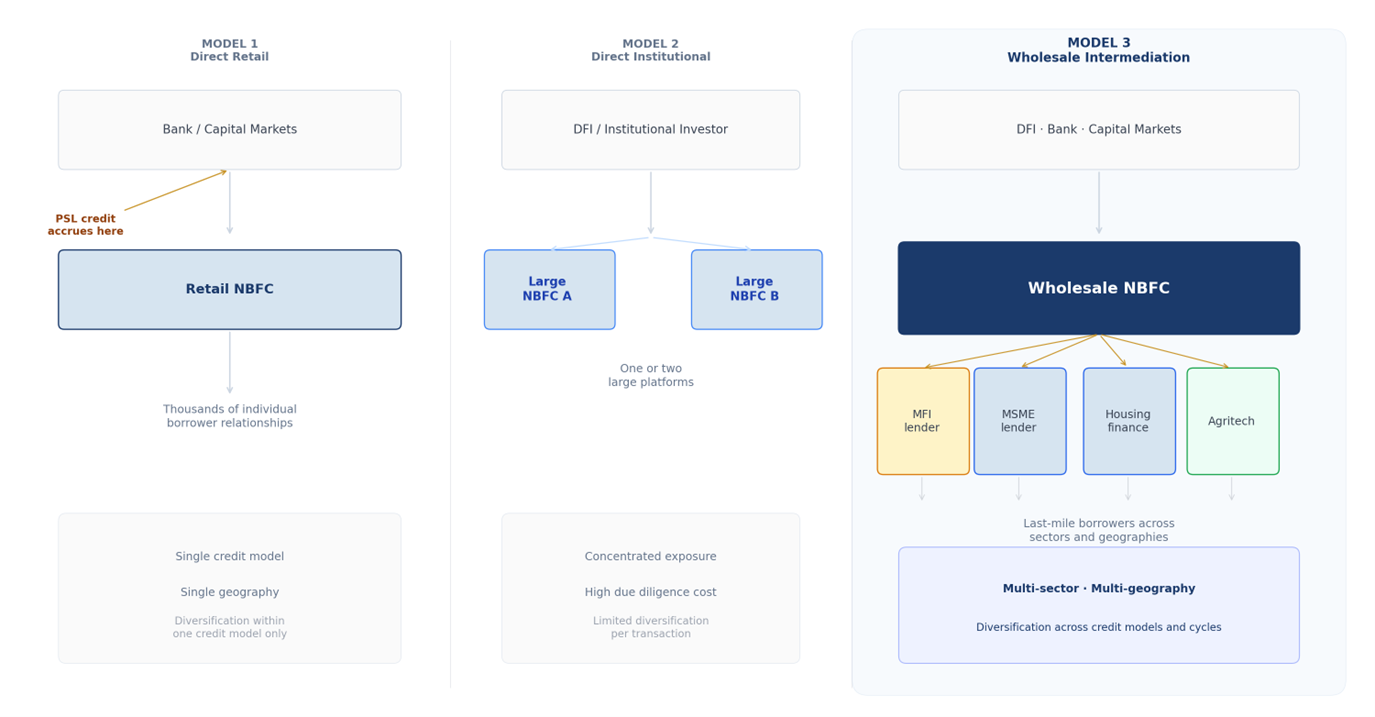

Exhibit 1: The Three Lending Models — Capital Chain and Credit Delivery. Structural illustration. PSL credit classification per RBI Master Directions on Priority Sector Lending 2025, Paras 22–24.

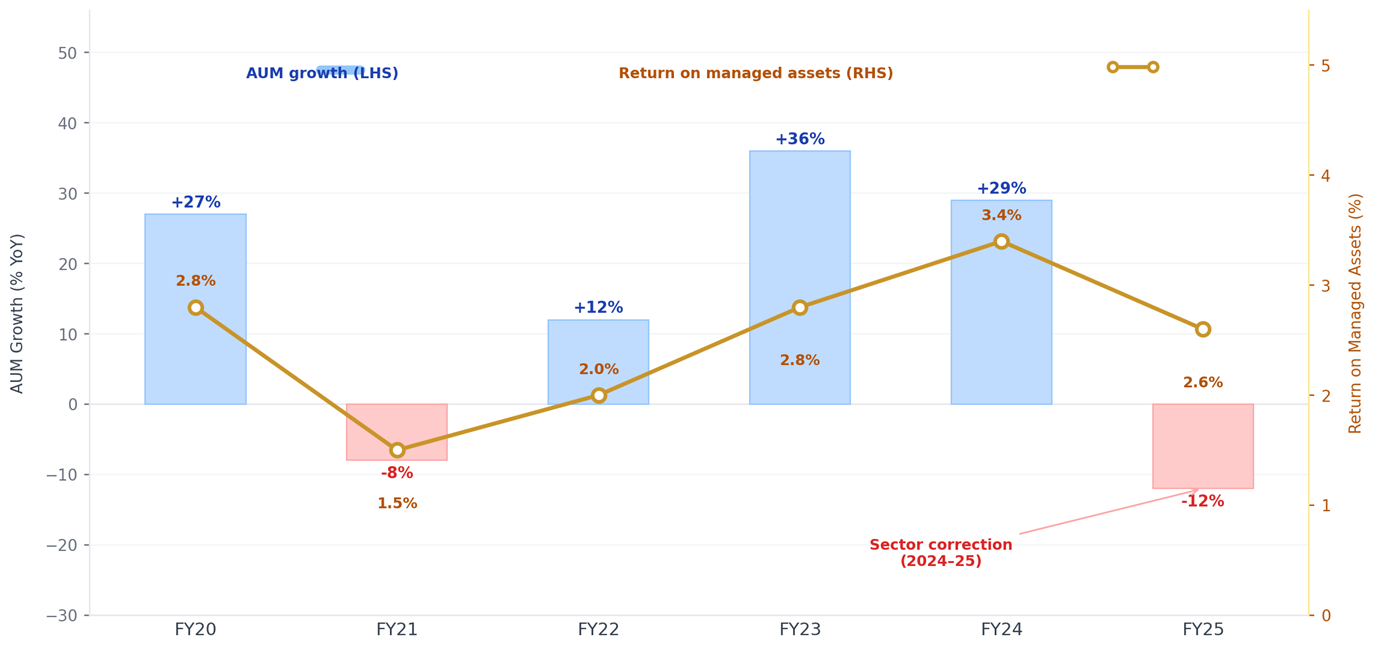

The structural constraints of the retail model are visible in the same ICRA data. The sector correction of 2024 to 2025 was severe by historical standards. NBFC-MFI AUM declined by 12%, reversing 29% growth in the prior year [8]. More telling was the asset quality deterioration: overall stress, measured as the sum of SMA, GNPA, write-offs and security receipts, surged to 15.3 percent of the opening book, versus 5.9 percent at March 2024. Provision coverage rose to approximately 4.8 percent of the on-book portfolio. The correction originated in borrower overleveraging and concentrated multi-lender exposure in specific geographies. When collections deteriorated, the impact was concentrated because the model’s geographic and borrower-segment exposure was concentrated. ICRA noted in its FY2025 assessment that NBFC-MFIs were actively managing the ratio of clients per field officer, with staff attrition exceeding 70% in some periods [8]. Retail credit at small ticket sizes scales through people and branches; that is the source of its reach and the limit of its operating leverage.

Exhibit 2: NBFC-MFI AUM Growth (YoY %) and Return on Managed Assets (%), FY2020–FY2025. Sources: ICRA NBFC-MFI Sector Reports FY2024 and FY2025. FY2021 AUM growth reflects pandemic disbursement disruption. FY2025 figures reflect ICRA reported actuals and projections as of July 2025.

None of this diminishes the importance of the retail model. It is the mechanism through which formal credit actually reaches the last mile, and no other model replicates its borrower relationship depth or community knowledge. The point is that its scaling characteristics impose constraints on how much institutional capital it can efficiently absorb before operational stretch and geographic concentration produce the kind of asset quality deterioration that the 2024 to 2025 correction illustrated.

Diversification through institutional intermediation

A wholesale NBFC lending to thirty regulated counterparties, each of which holds a diversified portfolio of retail borrowers in different geographies and sectors, achieves an effective exposure to the retail credit risk of millions of borrowers. That exposure arrives at the wholesale balance sheet already buffered and aggregated at the institutional level. A default event at a single counterparty is an institutional credit event, not the simultaneous deterioration of thousands of individual borrower relationships. The wholesale lender can assess and manage that risk using the same analytical tools applied to any institutional credit: financial statements, covenant structures, portfolio quality monitoring, and management engagement.

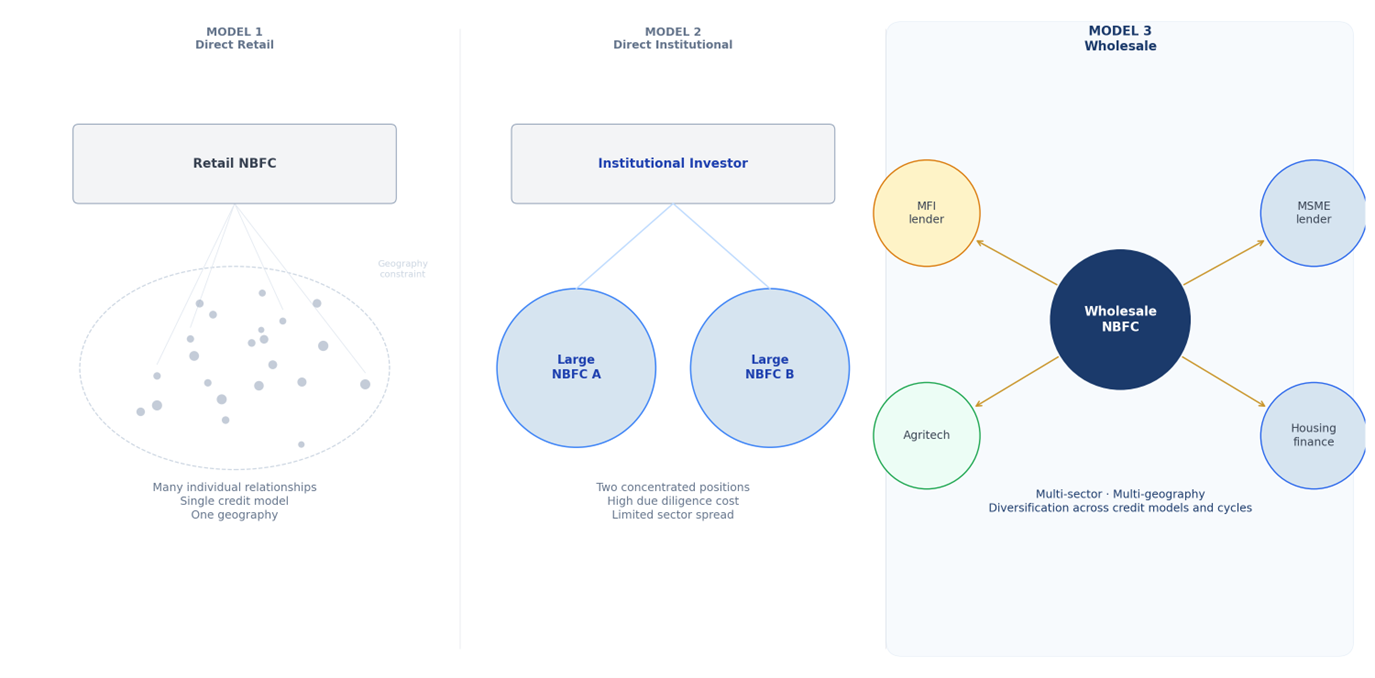

This is not the same diversification that a retail lender achieves by spreading across more borrowers. It is a different risk architecture. The retail lender’s diversification operates within a single model of credit risk: individual borrower income, household cash flow, local economic conditions. The wholesale lender’s diversification operates across models: its thirty counterparties may span microfinance, MSME lending, affordable housing, agritech and e-mobility, each with different demand drivers, different credit cycle sensitivities and different geographic concentrations. When the microfinance sector corrects, an MSME or housing finance counterparty is not necessarily under the same pressure. The cross-sector diversification is not incidental. It is a structural property of the multi-counterparty wholesale model.

Exhibit 3: Diversification Structure by Lending Model. Structural illustration. Counterparty types are indicative of sector practice. DFI model shown as two platforms for illustration; actual deployment varies.

Specialised underwriting that covers retail risk at institutional scale

The underwriting skill that the wholesale model requires is different from retail credit assessment. A retail credit officer assesses household income, the purpose of the loan, the borrower’s existing obligations and the local economic context. A wholesale credit officer assesses the institution: its governance, its credit culture, the quality and seasoning of its loan portfolio, its funding structure, its management depth, its regulatory standing and its behaviour under previous stress conditions.

This institutional assessment, when well executed, covers the credit risk of the entire retail portfolio the counterparty holds. The wholesale underwriter who assesses a microfinance institution’s portfolio quality, geographic concentration, borrower-level indebtedness management and collection infrastructure is effectively evaluating the credit risk of thousands of individual borrowers, but doing so at the institutional level through observable, auditable metrics rather than through direct borrower interaction. The same analytical capacity that underwrites one institutional counterparty covers more retail credit exposure than a field team of comparable size could directly manage.

The skill is harder to build than retail underwriting. It requires sector expertise, financial analysis capability and relationship depth with institutional counterparties that takes years to develop. But once built, it does not scale proportionately with portfolio size in the way that retail field infrastructure does. The team that underwrites thirty institutional counterparties can, with appropriate monitoring systems, manage a portfolio far larger than a retail credit team of equivalent headcount could directly originate and monitor. What the wholesale model cannot replicate is the retail lender’s direct knowledge of the borrower: the household assessment, the repayment culture, the community relationships that make last-mile credit possible in the first place. The two models are complements, not competitors.

Operating leverage from institutional ticket sizes

The third mechanism is the most straightforward arithmetically. A retail NBFC-MFI extending ₹50,000 average ticket loans to individual borrowers needs approximately 20,000 new loan relationships to grow its portfolio by ₹100 crore. Each of those relationships requires origination, documentation, disbursement and ongoing monitoring. A wholesale NBFC extending ₹25 to 200 crore institutional facilities to regulated NBFC counterparties needs two to four new relationships to achieve the same portfolio growth. The origination, documentation, disbursement and monitoring processes are more complex per transaction, but the transaction volume is orders of magnitude lower.

ICRA’s data on NBFC-MFI profitability illustrates the retail cost structure: return on managed assets of 3.2-3.4% in FY2024, with that figure reflecting the cost of a field-intensive, branch-dependent operating model [8]. The wholesale model does not have comparable published data by model type in public sources, because RBI supervisory data is published by SBR layer rather than by lending model within layers. What can be observed is structural: the absence of branch networks, field staff and retail collection infrastructure in the wholesale model means that operating costs do not grow with the portfolio in the same way.

Funding cost and spread architecture is a key disadvantage in the wholesale NBFC model worth exploring.

The wholesale NBFC operates in the middle of the capital chain, borrowing from banks and capital markets at rates that reflect its own credit standing, and lending to smaller NBFCs at a spread that must cover its operating costs, credit costs and return on equity. This intermediation layer carries an inherent spread cost that direct bank-to-NBFC lending does not. The wholesale model’s economic viability depends on whether its operating cost advantage over direct bank origination to multiple small NBFCs offsets the additional intermediation spread. Where the wholesale platform has genuine sector-specific underwriting depth and a diversified counterparty base, that cost advantage is real and the spread is justified by the institutional work the model performs. Where those conditions are absent, the case for the intermediation layer is weaker and platform-level due diligence should examine the cost trade-off directly.

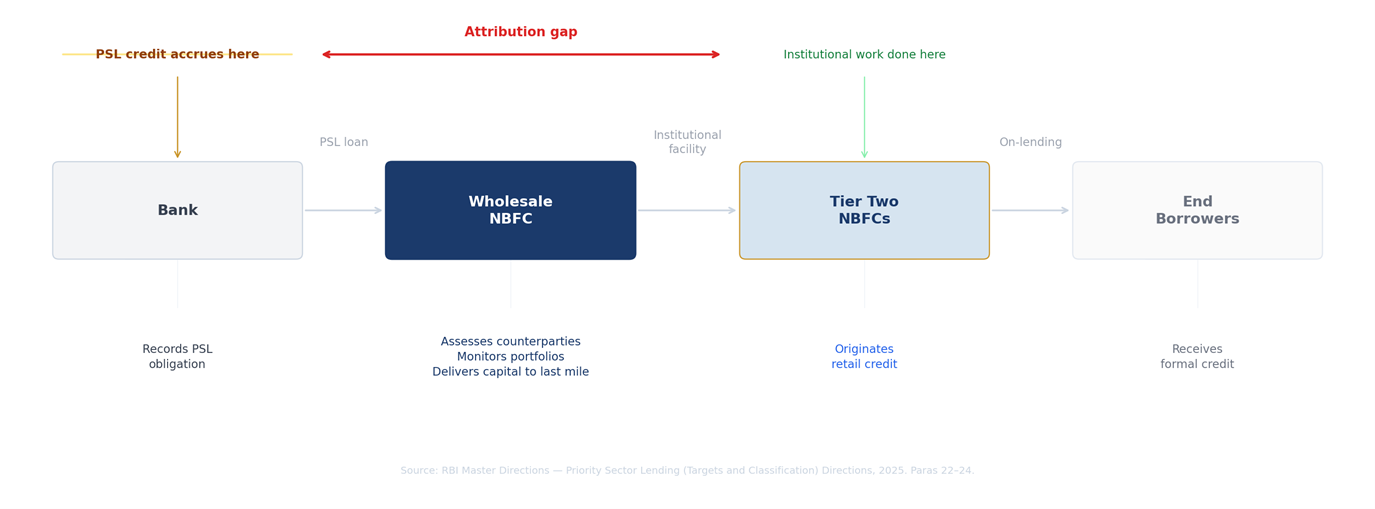

Exhibit 4: PSL Credit Chain — Attribution vs. Operational Contribution. Source: RBI Master Directions on Priority Sector Lending (Targets and Classification) Directions, 2025. Structural illustration of PSL classification mechanics under Paras 22–24.

“The PSL framework correctly assigns compliance responsibility to the bank as the regulated entity with the PSL obligation. The wholesale NBFC’s institutional contribution, the counterparty assessment, monitoring and on-lending that connects bank capital to last-mile borrowers, is part of the implementation chain that makes PSL deployment effective. Mapping that contribution precisely matters for understanding how financial inclusion outcomes are produced.”

The mechanics of this arrangement are straightforward and well-established. A bank lends to a wholesale NBFC. The wholesale NBFC lends to a portfolio of smaller NBFC counterparties. Those counterparties extend credit to microfinance borrowers, MSME owners, affordable housing customers and smallholder farmers who would not otherwise have access to formal credit. The bank’s loan to the wholesale NBFC qualifies for PSL classification, provided the end-use conditions are met. The bank records the PSL achievement. The wholesale NBFC records a liability.

What the PSL framework measures is credit outcomes at the point of bank deployment, which is the appropriate compliance point for a bank-facing regulatory instrument. The wholesale NBFC that assesses the creditworthiness of smaller NBFC counterparties, monitors their portfolio quality, structures the terms of the lending relationship and provides the institutional capital that allows them to lend to borrowers they would not otherwise reach is not the regulated entity with the PSL obligation. That work is nonetheless the mechanism through which the bank’s PSL capital reaches its intended beneficiaries. Understanding this distinction helps investors and policymakers map the full institutional contribution of each actor in the chain more precisely.

This asymmetry is not a regulatory error. The PSL framework measures credit outcomes at the point of bank deployment, not at the point of ultimate borrower impact. The bank is the regulated entity with the PSL obligation, and it is appropriate that the bank bears the compliance responsibility. What the framework does not measure is the institutional contribution of the intermediaries through whom that compliance is achieved. A bank that lends directly to a microfinance borrower through its own branch network and a bank that lends to a wholesale NBFC that lends to ten smaller NBFCs that collectively serve a hundred thousand microfinance borrowers receive the same PSL credit per rupee. The complexity, the institutional development work and the last-mile reach generated by the second arrangement are not reflected in the measurement.

This observation is not an argument for regulatory change. It is an analytical observation about how the wholesale model’s contribution to financial inclusion is currently measured, and therefore how it tends to be characterised in policy discussions. An investor or policymaker relying on PSL data alone to assess the role of different institutional actors in credit delivery will undercount the contribution of wholesale intermediaries. The credit gap this series has documented in earlier papers is not primarily a gap in bank PSL compliance. It is a gap in the institutional infrastructure that connects bank capital to last-mile borrowers. Wholesale NBFCs sit at the centre of that infrastructure.

Sources: ICRA NBFC-MFI Sector Reports [8]; RBI Priority Sector Lending Master Directions 2025 [1]; RBI SBR framework. Retail ticket size reflects MFIN data on average loan size. Wholesale facility size is indicative based on disclosed transaction data and sector practice. Profitability data for direct institutional and wholesale models is not published separately in public sources by lending model type. Characterisations marked as structural or definitional reflect the inherent design of each model rather than cited empirical data.

Several observations follow from the comparison. The diversification produced by the wholesale model is qualitatively different from retail diversification. A retail NBFC with a portfolio spread across 100,000 borrowers has granular diversification within a single credit model. A wholesale NBFC with thirty institutional counterparties spanning five sectors has diversification across credit models and credit cycles, which is a more resilient risk architecture under systemic stress.

The operating cost driver for each model also follows from the architecture. The retail model’s operating costs scale with the portfolio because origination, monitoring and collections are people-intensive and cannot be centralised without losing the local knowledge that makes the model work. The wholesale model’s operating costs grow more slowly because the critical work is institutional analysis rather than field-level borrower management. ICRA’s observation that NBFC-MFIs were managing the ratio of assets per field officer, and that staff attrition exceeded 70 percent in stress periods, is a concrete illustration of the operational intensity that the retail model requires [8]. The wholesale model faces different operational challenges, but they are analytical rather than logistical.