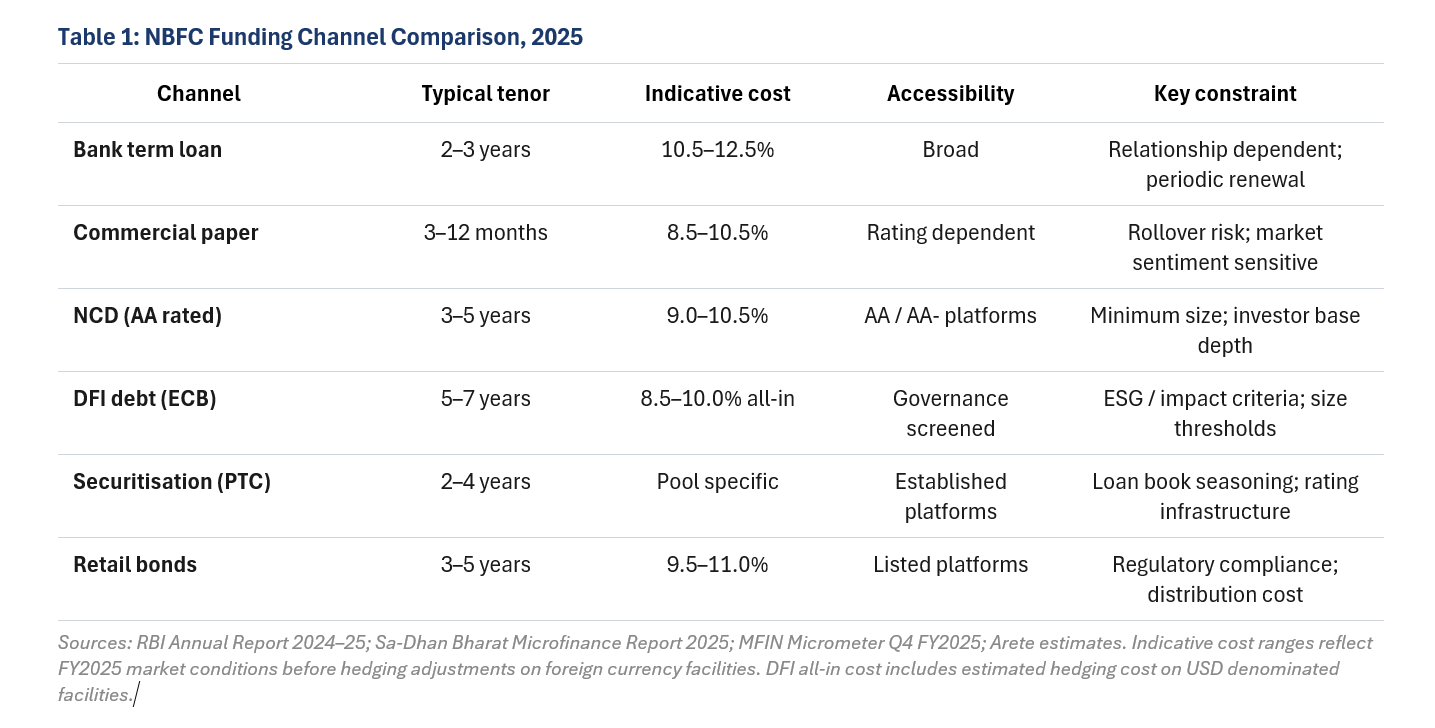

Development finance institution debt

The IFC, DEG, FMO, Proparco, the Asian Infrastructure Investment Bank and several bilateral development lenders have increased their India financial inclusion exposure substantially since 2018. For NBFC counterparties that meet their eligibility criteria, DFI debt carries two advantages beyond the headline rate. Tenor is typically five to seven years, significantly longer than the two to three year domestic bank term loan that remains the default for most platforms. And pricing, after accounting for hedging costs on foreign currency denominated facilities, typically runs 50 to 150 basis points below comparable domestic term loan rates in periods when the USD/INR forward premium is moderate; in periods of elevated forward costs the advantage narrows and can be eliminated. That spread is not trivial at the scale of an NBFC balance sheet. On a ₹500 crore DFI facility, a 100 basis point cost advantage over a domestic term loan represents ₹5 crore of annual interest saving that either flows to lending margin or is passed through to borrowers as lower rates.

The eligibility criteria are the constraint. DFI lenders typically require environmental, social and governance assessment, impact measurement frameworks aligned with recognised international standards, board-level governance structures that can withstand external scrutiny, and credit standards that most sub-₹500 crore platforms have not yet fully built. Access is conditional on institutional maturity, not just credit quality. That conditionality is deliberate. It creates a selection effect that concentrates concessional long-tenor capital in platforms that have demonstrated the capacity to deploy it responsibly.

Domestic capital markets

The non-convertible debenture market has deepened considerably as an NBFC funding channel since 2019. Rated NCD issuances by established NBFC platforms now attract insurance companies, pension funds, mutual funds and corporate treasuries seeking credit exposure above the sovereign curve. For platforms with AA or AA minus ratings, the market is liquid and pricing is competitive. The development is significant because NCD funding, unlike bank term loans, is not subject to the relationship dynamics and periodic renegotiation that make bank credit management operationally intensive. A five year NCD at a fixed spread provides funding visibility that a bank term loan renewed annually does not.

Retail bond issuances have also become viable for a subset of platforms. Several NBFC-MFIs and housing finance companies have placed bonds directly with retail investors through the BSE and NSE platforms, diversifying their funding base beyond the institutional investor community. The volumes remain modest relative to total funding requirements, but the channel matters because it demonstrates public market access, which in turn supports credit rating stability and institutional investor confidence.

External commercial borrowings

ECB access has expanded for NBFCs in eligible end-use categories, including affordable housing, microfinance and renewable energy lending. For platforms that qualify, the all-in cost after hedging has been competitive with domestic alternatives in periods of favourable forward curve conditions. More importantly, ECB facilities from DFI lenders frequently carry technical assistance components and covenant structures that help platforms build the institutional infrastructure that sustains their rating and their access to further capital. The ECB channel is therefore not purely a funding transaction. For many platforms it has been an institutional development relationship as much as a liability management exercise.

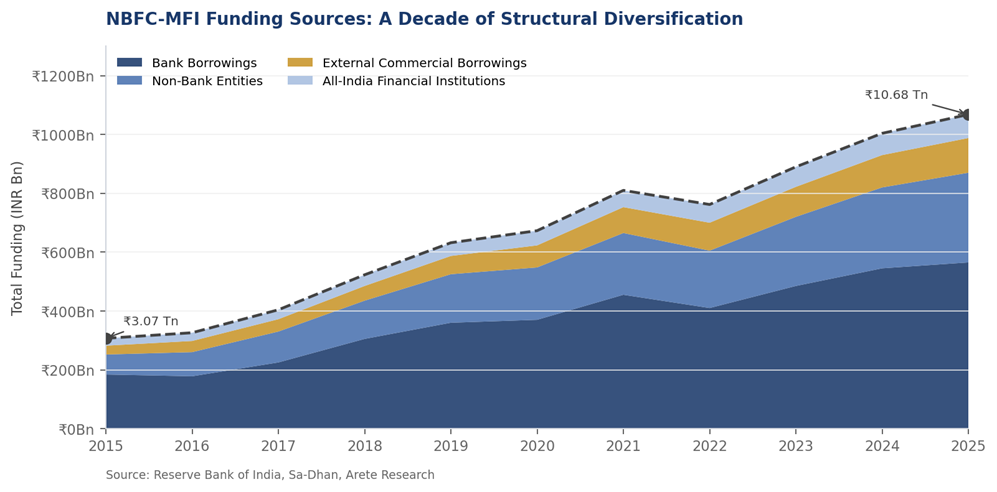

The chart below, drawn from RBI NBFC return submissions compiled by Sa-Dhan, illustrates the compositional shift in NBFC-MFI funding sources between 2015 and 2025. Bank borrowings, which constituted the dominant share of funding in the earlier period, have been displaced progressively by NCD issuances, securitisation and external borrowings. The shift is not uniform across the sector. It reflects the growing weight of larger, better-rated platforms whose funding diversification pulls the aggregate composition. For smaller platforms the picture is different, and that difference is the subject of the following section.

Exhibit 1: NBFC-MFI Funding Sources, Composition and Growth, 2015 to 2025 (INR Billion). Source: RBI NBFC return submissions as compiled by Sa-Dhan Annual Bharat Microfinance Report 2025. Data covers NBFC-MFI entities reporting to the RBI and reflects the MFI segment; it does not capture the full NBFC universe.

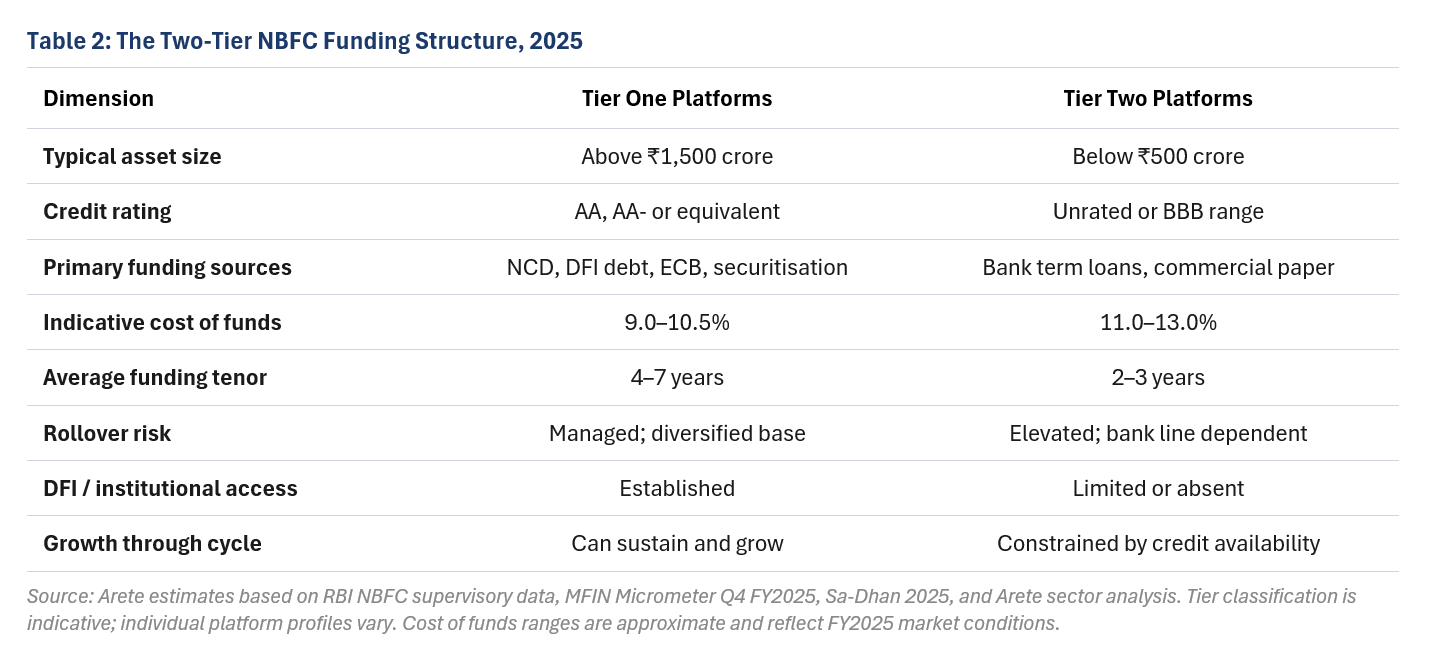

The trap has a specific mechanism. A regulated NBFC with assets of ₹300 crore, a sound loan book and three years of consecutive profitability cannot access DFI debt because its asset size falls below the minimum ticket size that makes DFI due diligence economically viable. It cannot issue NCDs because it lacks rating infrastructure and investor relationships that NCD placement requires. It cannot securitise at scale because its loan book lacks the seasoning and standardisation that rating agencies require for investment-grade structured credit. It therefore remains on bank term loans at 11 to 12.5 percent, renewing them every two to three years, managing its growth trajectory around bank credit availability rather than borrower demand availability.

Growing out requires capital the platform cannot access until it has grown. The circularity is the defining feature of the trap. Platforms that escape it typically do so through one of three routes: a strategic equity investor who provides the capital injection that crosses the rating threshold; a DFI that grows an early-stage relationship as the platform matures; or a wholesale NBFC counterparty whose lending provides the liability that helps the borrowing NBFC build balance sheet scale. Each route depends on a relationship, a judgment call by a capital provider that the platform is worth backing before the metrics fully justify it. The opportunity for the next phase of sector development lies in making those relationships more systematic, extending the benefits of institutional capital access to a broader set of platforms through structured mechanisms that complement what the market generates on its own.

“The borrower who takes a loan from a Tier Two NBFC is likely to pay more than a borrower of comparable creditworthiness served by a Tier One platform. That difference is not a reflection of borrower risk. Closing it is the central challenge and the central opportunity for the next phase of India’s financial inclusion agenda.”

The cycle is self-reinforcing and it operates in both directions. When credit conditions tighten, as they did in 2018 to 2019 and again during the MFI sector correction of 2024 to 2025 [6][7], Tier Two platforms face disproportionate funding pressure. Commercial paper markets price in sector sentiment broadly, without always distinguishing between well-run and poorly-run platforms, because the rating and track record infrastructure that enables that distinction takes time to build. Platforms serving geographically remote or financially excluded borrowers are therefore most exposed to funding volatility, which is precisely why building institutional resilience in those platforms is an important policy and market objective. The borrowers in these segments benefit the most when the platforms serving them can sustain access through periods of market stress.

This is not a cyclical problem that corrects itself automatically when credit conditions improve. When conditions improve, Tier One platforms benefit first and most, deepening the funding advantage that the stress period has already widened. Tier Two platforms recover more slowly, and the sector correction of 2024 to 2025 has produced a consolidation dynamic in which some smaller platforms are ceding market share to larger ones. That consolidation is not inherently bad for borrowers if the acquiring platform serves them at lower cost. It does, however, reinforce the importance of maintaining a diverse institutional ecosystem. India’s financial inclusion agenda has been built on the strength of platforms with deep geographic reach and sector-specific expertise, and preserving that diversity alongside scale is the defining challenge for the sector’s next phase.

The scale of the trapped segment

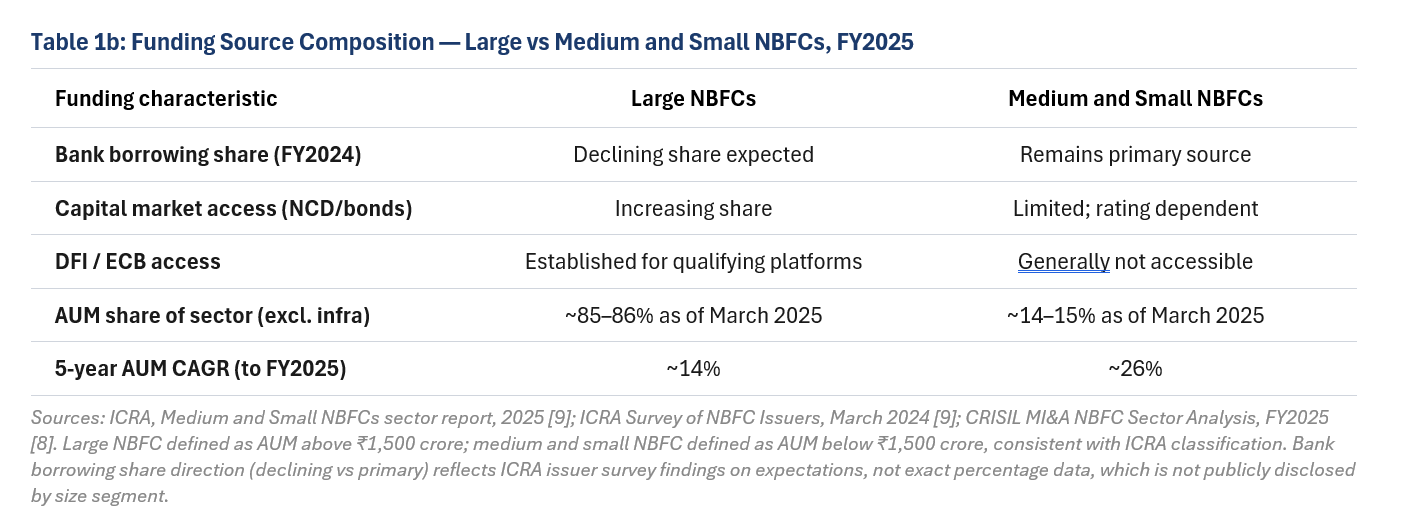

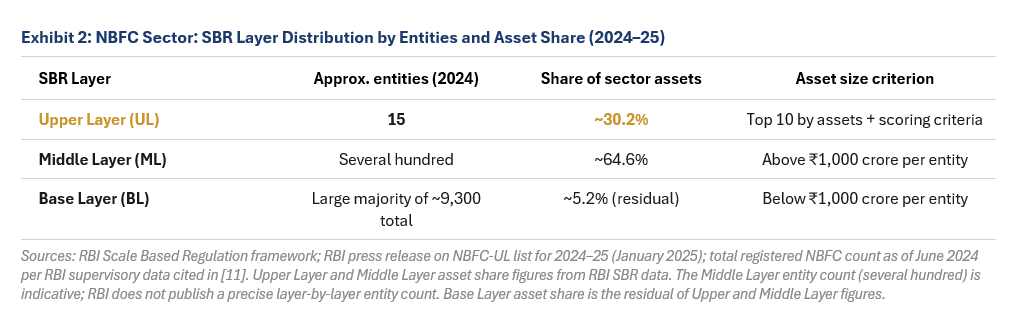

The RBI’s Scale Based Regulation framework provides the clearest available proxy for the size of the trapped segment. As of June 2024, approximately 9,300 NBFCs were registered with the Reserve Bank [11]. Of these, 15 were classified in the Upper Layer for 2024–25, identified by the RBI as warranting enhanced regulatory oversight based on size and a scoring methodology. The Upper Layer entities collectively account for approximately 30.2 percent of total NBFC sector assets. The Middle Layer, comprising deposit-taking NBFCs of all sizes and non-deposit-taking NBFCs with assets above ₹1,000 crore per entity, accounts for approximately 64.6 percent of sector assets. The Base Layer, consisting of non-deposit-taking NBFCs with assets below ₹1,000 crore, contains the large majority of registered entities by number but a residual share of total assets [5].

ICRA’s assessment of medium and small NBFCs, defined as those with AUM below ₹1,500 crore, found that this segment accounted for approximately 14 to 15 percent of total NBFC sector AUM as of March 2025, despite growing at a five-year compound annual rate of approximately 26 percent, materially faster than the 14 percent recorded by larger peers over the same period [10]. This combination, faster loan book growth alongside a funding base that does not diversify in the way larger platforms can, is consistent with the dynamic the funding trap describes. ICRA’s 2024 survey of NBFC issuers found that larger entities expected bank funding to decline as a share of their mix, while smaller peers expected bank borrowings to remain their primary funding source [10]. The divergence is not new, but the data suggest it is not narrowing.

The table below sets out the SBR layer distribution. The figures are drawn from RBI supervisory data and illustrate the structural asymmetry: 15 Upper Layer entities account for nearly a third of all NBFC sector assets, while the large majority of registered NBFCs by number sit in the Base Layer, below the asset thresholds at which institutional capital markets become accessible.

Asset quality divergence by lender size

India’s NBFC sector demonstrated considerable overall resilience through the FY2025 microfinance correction, reflecting the stronger funding and governance foundations built since 2018. Within that broader resilience, however, the stress was not evenly distributed. MFIN data for Q4 FY2025 shows PAR30+ at 8.1% for smaller NBFC-MFIs, compared to materially lower levels reported by larger NBFC-MFIs that benefited from diversified funding, stronger collection infrastructure, and the capacity to manage stressed portfolios more actively. This pattern is consistent with the feedback loop described above: platforms operating at higher cost of funds and thinner margins have less capacity to absorb stress, which reinforces the case for extending institutional funding access further down the size distribution.